Cash Request Online Review: Deep Dive into Rates, Fees, and Risks (2026)

Contents show

1 Cash Request Online Review: Deep Dive into Rates, Fees, and Risks (2026)

High-Risk Financial Warning: Payday loans and short-term credit products carry extremely high Annual Percentage Rates (APR) and are intended only for dire financial emergencies. They are not suitable for long-term financial solutions or discretionary spending. Borrowers should exhaust all other alternatives—such as credit union loans, personal lines of credit, or assistance programs—before engaging with high-interest debt instruments.

In the 2026 American financial landscape, the “payday loan” has evolved from a storefront operation into a complex digital ecosystem of algorithmic intermediaries. Cash Request Online represents a prominent example of a connection service, or lead generator, operating in the high-risk consumer credit segment.

As a Your Money Your Life (YMYL) topic, understanding the mechanism behind Cash Request Online is critical for consumer protection. This service does not lend money directly; rather, it serves as a digital gateway, capturing sensitive consumer data and auctioning it to a network of third-party lenders. This report provides an independent analysis of the service’s operational model, the real-world cost of its products, and the regulatory environment governing its partners in 2026.

| Feature | Details |

| Service Type | Lead Generator / Connection Service |

| Loan Amounts | Typically $100 to $5,000 (varies by lender) |

| Estimated APR Range | 200% to 600%+ |

| Turnaround Time | Often as fast as the next business day |

| Credit Impact | Usually “No Hard Pull” for initial request |

| State Availability | Subject to individual state legislation |

Cash Request Online functions as a marketing platform rather than a financial institution. To establish trust in the YMYL category, it is essential to note that lead generators often operate under multiple brand names to manage their digital reputation. While the service provides a streamlined interface for those with limited credit options, users must recognize that they are not entering into a contract with Cash Request Online itself, but with an undisclosed third-party lender.

Cash Request Online utilizes an automated real-time auction system known as a “Pingtree.” When a user submits an application, the following technical sequence occurs:

Data Harvesting: The service collects extensive personal information, including Social Security Numbers (SSN), employment details, and active bank account routing numbers.

The Auction (The Ping): The user’s data “lead” is offered to a network of lenders. These lenders use proprietary algorithms to evaluate the risk and bid on the lead.

The Redirect: The consumer is automatically redirected to the website of the lender who won the auction—typically the one willing to pay the highest price for the lead.

Analytical Insight: This model often creates a conflict of interest. The lender who pays the most for a lead is frequently the one with the highest interest rates, as they need larger profit margins to offset the cost of acquiring the customer.

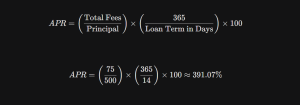

The most critical component of evaluating Cash Request Online is the mathematical deconstruction of the loans offered by its partners. In 2026, transparency regarding the Annual Percentage Rate (APR) remains the primary defense against debt traps.

Payday loans are often marketed with “flat fees” (e.g., “$15 per $100 borrowed”). However, to compare this to other financial products, one must convert this fee into an APR.

Calculation Example:

If a borrower takes out a $500 loan for a 14-day term with a $15 fee per $100 ($75 total fee):

In deregulated states like Idaho or Texas, where additional service fees are common, the APR can exceed 600%.

Partner lenders accessed via Cash Request Online typically employ a multi-layered fee structure :

Origination Fees: A one-time charge for processing the loan, usually 1% to 5%.

Non-Sufficient Funds (NSF) Fees: Charged if the lender attempts to withdraw a payment and the account balance is too low.

Rollover Fees: The cost of extending the loan for another term. This is the primary driver of the “debt cycle,” where the borrower pays interest only and never reduces the principal.

The legality and cost of using Cash Request Online are dictated entirely by the borrower’s state of residence and federal protections enforced by the Consumer Financial Protection Bureau (CFPB).

A landmark regulation that remains central in 2026 is the CFPB’s rule on failed payment attempts.

The Rule: Lenders are prohibited from making more than two consecutive attempts to withdraw funds from a borrower’s account if previous attempts failed due to insufficient funds.

The Protection: To make a third attempt, the lender must obtain new, specific authorization from the consumer. This prevents a cascade of $35 bank NSF fees that can deplete a borrower’s remaining income.

As of 2026, the U.S. is divided into three distinct regulatory zones :

Strictly Regulated (36% APR Cap): States like Illinois, New York, and New Jersey have effectively banned traditional payday lending by imposing a 36% ceiling.

Hybrid/Tiered Regulation: States like Colorado (~114% APR) allow higher rates but limit total interest and prohibit certain predatory practices.

Deregulated Markets: In Texas or Idaho, the use of Credit Services Organization (CSO) models allows lenders to bypass interest caps through unlimited “service fees,” resulting in APRs over 600%.

Military Protection: Under the Military Lending Act (MLA), active-duty service members and their families are protected by a federal 36% MAPR cap. Any loan exceeding this for a covered borrower is legally void.

Cash Request Online targets “subprime” borrowers who are often excluded from the traditional banking system.

While requirements vary by lender, the general baseline in 2026 includes:

Income Verification: Evidence of at least $800–$1,000 in monthly income (via paystubs or direct deposit).

Active Checking Account: Most lenders require an account that has been open for 90+ days and is not currently in a negative balance.

Identity: A valid Social Security Number (SSN) and U.S. residency.

During the application, users are often asked to provide bank credentials via services like Plaid for real-time transaction analysis. While this speeds up approval, it gives lenders deep insight into the borrower’s spending habits. Furthermore, because the site is a lead generator, your contact information may be shared with marketing partners, leading to an increase in unsolicited financial offers.

Requesting funds via a connection service follows a specific digital workflow designed for speed and data capture.

Submit the Online Request: Complete the primary form on CashRequestOnline.com. You will need to provide your legal name, address, Social Security Number, and details about your regular income.

Automatic Pingtree Auction: Once submitted, your data is instantly shared with a network of lenders in an automated auction. The system “pings” multiple lenders to find one willing to accept your application based on their internal risk algorithms.

Review the Matched Offer: If a lender accepts your request, you will be automatically redirected to their specific website. Here, the lender is required to show you the specific loan amount, interest rate, and APR before you commit.

E-Sign the Agreement: Carefully read the loan contract. If you agree to the terms, you will sign the document electronically. Note that at this stage, you are dealing directly with the lender, not Cash Request Online.

Fund Disbursement: After final approval, funds are typically sent via ACH direct deposit to your bank account. Depending on the lender and your bank’s processing times, this often occurs within 24 hours or by the next business day.

Because Cash Request Online is not the lender, the repayment process occurs directly between you and the company that disbursed the funds.

Identify Your Lender: Locate your signed loan agreement or check your email for the welcome packet from the third-party lender. All payments must be coordinated through their platform.

Set Up Automatic Payments (ACH): Most lenders in this network default to automatic withdrawals. Ensure that the required funds are in your checking account by the morning of your due date (typically your next payday).

Monitor Withdrawal Attempts: If you lack sufficient funds, be aware of the “Two-Strikes” rule. Your lender can only attempt to debit your account twice. If both fail, they cannot try again without your renewed permission.

Request an Extended Payment Plan (EPP): If you cannot make the full payment, check if your state requires the lender to offer an interest-free EPP. In many states, you must request this at least one business day before the loan is due.

Confirm Loan Closure: Once the final payment is made, verify with the lender that your balance is zero. Keep a copy of the payment confirmation to prevent errors or unauthorized future debits.

Analysis of customer sentiment on platforms such as Trustpilot and Reddit indicates a polarized experience.

Positive Feedback: Users typically praise the speed of the process and the ability to cover immediate costs like car repairs or medical bills when no other options were available.

Common Complaints: Negative reviews frequently cite a barrage of marketing calls and emails following the application. Others express confusion when the final loan terms (APR and fees) are significantly higher than the “representative examples” shown on the initial landing page.

Reputation Alert: The lead generation industry is subject to “Review Rackets,” where some platforms may prioritize or suppress reviews based on business relationships. Investors and consumers should weigh Trustpilot scores with a “grain of salt.”

Before proceeding with a request through Cash Request Online, borrowers should consider these significantly lower-cost alternatives available in 2026:

Offered by many federal credit unions, PAL II loans are designed specifically to break the payday debt cycle.

Max APR: 28%.

Loan Amount: Up to $2,000.

Requirement: Must be a member of the credit union (many offer immediate online membership).

Apps like Earnin, Dave, or Brigit offer small advances on earned wages.

Cost: Often 0% APR, relying on “tips” or small monthly subscriptions rather than interest.

Constraint: Limits are usually lower ($100–$500) and tied directly to your upcoming paycheck.

| Parameter | Cash Request Online | PAL II (Credit Union) | Traditional Credit Card | Cash Advance App |

| APR | 300% – 600%+ | Max 28% | 18% – 30% | 0% + Tips |

| Speed | 24 Hours | 1–3 Days | Immediate | Immediate |

| Credit Check | No Hard Pull | Soft/Hard Pull | Hard Pull | No Hard Pull |

| Term | 14–30 Days | 1–12 Months | Revolving | Next Payday |

Alabama

Alabama Alaska

Alaska Arizona

Arizona California

California Colorado

Colorado Delaware

Delaware District of Columbia

District of Columbia Florida

Florida Hawaii

Hawaii Idaho

Idaho Illinois

Illinois Indiana

Indiana Iowa

Iowa Kansas

Kansas Kentucky

Kentucky Louisiana

Louisiana Maine

Maine Maryland

Maryland Massachusetts

Massachusetts Michigan

Michigan Minnesota

Minnesota Mississippi

Mississippi Missouri

Missouri Montana

Montana Nebraska

Nebraska Nevada

Nevada New Jersey

New Jersey New Mexico

New Mexico North Carolina

North Carolina North Dakota

North Dakota Ohio

Ohio Oklahoma

Oklahoma Oregon

Oregon Pennsylvania

Pennsylvania Rhode Island

Rhode Island South Carolina

South Carolina Tennessee

Tennessee Texas

Texas Utah

Utah Virginia

Virginia Washington

Washington Wisconsin

Wisconsin Wyoming

WyomingCash Request Online serves as a high-speed, high-cost bridge for individuals facing immediate financial crises who have no access to traditional credit. While the technology provides a seamless user experience, the underlying financial products are among the most expensive in the global market.

Who is this for? It is a tool of last resort for those facing a “true emergency”—such as the risk of utility disconnection or a car repair required for employment—who do not qualify for a PAL II or a cash advance app.

Who is it NOT for? It should never be used for non-essential purchases, holiday spending, or to pay off other existing high-interest debt.

Final Verdict: Approach with extreme caution. The “Pingtree” model prioritizes lender profit over borrower affordability. If you must use this service, have a guaranteed plan to repay the principal in full on your next payday to avoid the catastrophic effects of the rollover cycle.

For more information, visit their official website at Cash Request Online.

Michael Turner is a financial editor and credit analyst specializing in consumer lending in the United States. He has over 8 years of experience analyzing payday loans, installment loans, and alternative credit products.

His work focuses on real borrowing costs, APR calculations, penalties, rollover conditions, and borrower risk scenarios. Michael reviews loan offers across different U.S. states with attention to regulatory disclosures and consumer protection.

Language: English

Region focus: United States