Psychology of Money and Behavioral Finance Explained

Contents show

Views: 196

Introduction

Money decisions are rarely purely rational. While financial theory often assumes that people act logically, real-world behavior consistently proves otherwise. Individuals regularly overspend, underestimate risk, avoid saving, or take on debt despite understanding the potential consequences.

Behavioral finance and the psychology of money examine why people behave the way they do with money, how emotions and cognitive biases affect decisions, and why financial knowledge alone is often insufficient to change outcomes.

This hub page provides a structured, independent overview of how psychology interacts with finance — helping readers recognize patterns, reduce harmful behaviors, and approach financial decisions more consciously.

What Is the Psychology of Money?

The psychology of money studies how beliefs, emotions, experiences, and social influences shape financial behavior. It focuses on:

- Spending habits

- Saving behavior

- Risk tolerance

- Debt decisions

- Investment choices

- Reactions to financial stress

These factors operate continuously, often outside conscious awareness.

What Is Behavioral Finance?

Behavioral finance is a field that combines psychology and economics to explain why real people deviate from “rational” financial models. It studies predictable behavioral patterns such as:

- Overconfidence

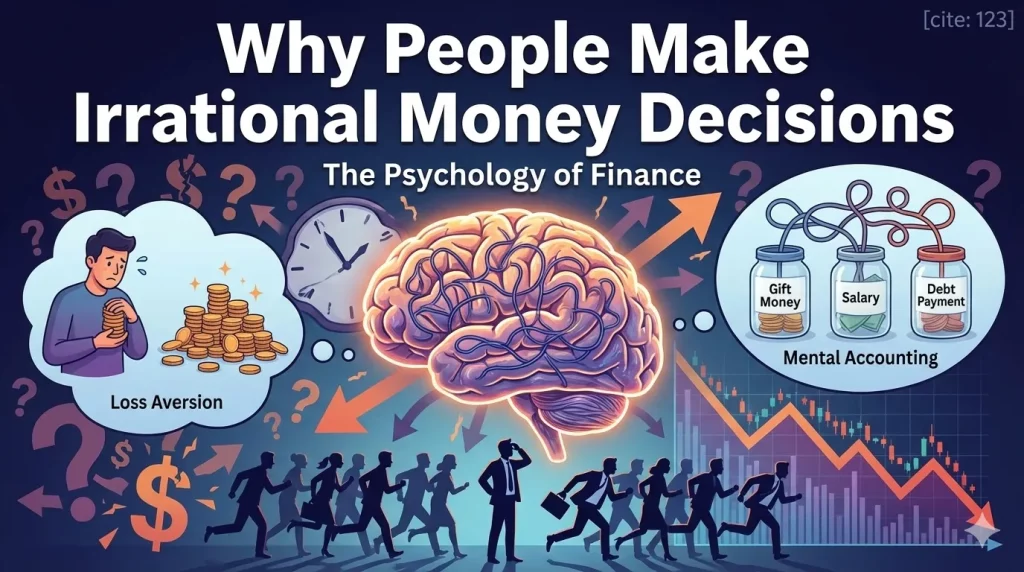

- Loss aversion

- Herd behavior

- Anchoring

- Mental accounting

Behavioral finance explains why markets and personal finances behave inconsistently with purely logical models.

Rational vs Real-World Financial Behavior

Traditional finance assumes:

- People maximize utility

- Decisions are consistent

- Information is processed logically

In reality:

- Emotions influence timing

- Decisions change under stress

- Short-term feelings override long-term goals

Understanding this gap helps explain why financial plans often fail in practice.

How traditional banking works → Banking, Payments and Accounts

Emotional Drivers of Financial Decisions

Fear

Fear leads to:

- Avoiding investments

- Panic selling

- Over-saving

- Delaying decisions

Greed

Greed can cause:

- Excessive risk-taking

- Overconfidence

- Chasing returns

- Ignoring warning signs

Stress

Financial stress reduces cognitive capacity and increases impulsive behavior.

Cognitive Biases That Affect Money Decisions

Loss Aversion

People feel losses more strongly than gains of equal size, leading to overly conservative behavior or reluctance to accept necessary losses.

Anchoring

Initial numbers influence decisions even when irrelevant (e.g., first loan offer or interest rate seen).

Confirmation Bias

People seek information that confirms existing beliefs and ignore contradictory evidence.

Present Bias

Immediate rewards are prioritized over long-term benefits.

Habit Formation and Financial Behavior

Most financial actions are habitual:

- Daily spending

- Subscription usage

- Saving patterns

- Payment behavior

Habits form automatically and persist until consciously changed. Financial education alone rarely breaks entrenched habits.

Budgeting and habit formation → Personal Finance and Budget Management

Money Beliefs and Upbringing

Early experiences shape:

- Attitudes toward debt

- Comfort with spending

- Perception of risk

- Views on wealth and scarcity

Beliefs formed in childhood often persist unconsciously into adulthood.

Social Influence and Money

Social factors influence:

- Lifestyle inflation

- Spending norms

- Investment trends

- Borrowing behavior

Comparison with others frequently drives financial decisions more than actual needs.

How credit systems work → Credit History and Scoring

Behavioral Aspects of Borrowing

Borrowing decisions are affected by:

- Immediate needs

- Optimism bias

- Underestimating repayment difficulty

- Emotional relief from short-term solutions

This explains why individuals may repeatedly use high-cost borrowing despite negative experiences.

Borrowing mechanisms explained → Loans and Borrowing

Behavioral Biases in Investing

Common patterns include:

- Panic selling during downturns

- Overtrading

- Herd investing

- Chasing past performance

Behavioral mistakes often have a larger impact on returns than market conditions.

Investment fundamentals → Investments and Savings

Money, Identity, and Self-Worth

For many people, money is linked to:

- Status

- Security

- Control

- Self-esteem

Financial difficulties may trigger shame or avoidance rather than problem-solving.

Financial Stress and Decision Quality

Stress impairs:

- Long-term planning

- Risk assessment

- Information processing

Under pressure, people default to familiar or emotionally comforting behaviors, even if harmful.

Digital Finance and Behavioral Triggers

Online platforms increase:

- Spending frequency

- Impulse purchases

- Subscription accumulation

- Borrowing speed

Reduced friction amplifies behavioral biases.

Digital behavior and finance → Online Finance and Fintech

Behavioral Tools for Better Financial Decisions

Helpful approaches include:

- Cooling-off periods

- Automation of savings

- Pre-commitment strategies

- Simplified choice environments

- Reflection before major decisions

These tools work by shaping behavior rather than relying on willpower.

Psychology and Financial Education

Effective financial education integrates:

- Emotional awareness

- Behavioral design

- Practical systems

- Long-term habits

Pure information delivery rarely changes outcomes.

Role of Behavioral Finance in Financial Planning

Behavioral insights improve:

- Goal realism

- Risk alignment

- Plan adherence

- Stress management

Planning should adapt to human behavior rather than assume ideal rationality.

Educational Scope and Independence

Fast Express Money does not provide therapy, coaching, or personalized advice. This section offers independent, educational insight into how psychology affects financial outcomes.

Focus areas:

- Awareness

- Responsibility

- Informed decision-making

- Long-term stability

Articles in This Category

This hub page connects to:

- Spending behavior analysis

- Debt psychology guides

- Risk perception articles

- Financial stress management

- Decision-making frameworks

(Content displayed dynamically.)

Frequently Asked Questions (FAQ)

Why do people repeat the same financial mistakes?

Can financial knowledge overcome bad habits?

Is fear always harmful in finance?

Do emotions affect professional investors?

Can behavioral finance improve financial outcomes?

Conclusion

The psychology of money explains why financial outcomes often differ from intentions. Understanding emotions, biases, and habits allows individuals to approach money with greater awareness and resilience.

Financial stability is not achieved by eliminating emotion — but by recognizing and managing it.

This hub page provides a foundation for understanding money as both a financial and psychological system.

Author

Financial Editor & Credit Analyst

Areas of expertise:

Payday loans and short-term credit

Installment loan structures

APR, fees, and penalties

State-level lending regulations

Borrower risk analysis

Michael Turner is a financial editor and credit analyst specializing in consumer lending in the United States. He has over 8 years of experience analyzing payday loans, installment loans, and alternative credit products.

His work focuses on real borrowing costs, APR calculations, penalties, rollover conditions, and borrower risk scenarios. Michael reviews loan offers across different U.S. states with attention to regulatory disclosures and consumer protection.

Areas of expertise:

Payday loans and short-term credit

Installment loan structures

APR, fees, and penalties

State-level lending regulations

Borrower risk analysis

Language: English

Region focus: United States